The European Union's flagship pandemic recovery fund, the Recovery and Resilience Facility (RRF), suffers from unacceptable gaps in the traceability and transparency of spending, according to a recent audit report by the European Court of Auditors (ECA).

Created in February 2021 and managed by the European Commission, the RRF is an emergency programme to help EU countries recover from the Covid-19 crisis and build resilient economies. By the end of January 2026, the Commission had committed a total of €577 billion to all EU Member States: €360 billion in grants and €217 billion in loans.

In previous audits, the ECA criticised the "accountability gap" in the RRF. This time, it focused on the "transparency gap" and shortcomings in the traceability of the costs. Public information on recipients of money, actual costs of measures and results achieved is insufficient because the RRF model of financing is not linked to actually incurred costs, as in the EU's regular spending programmes, according to the report.

Instead, the EU decided, under pressure of the crisis, to finance reforms and investments under the RRF based on the fulfilment of pre-defined milestones and targets. This is the first time the EU has used financing not linked to costs on such a large scale.

"Citizens have less trust in public finances if money is not spent with full transparency," said Ivana Maletić, the Croatian ECA Member leading the audit, at a virtual press briefing (6 May) about the audit report.

“We do not have a complete picture of how RRF funds are used. Citizens have the right to know how public funds are used, who receives the funds, and how much is actually spent," she said.

These RRF transparency gaps should not spill over into the EU’s future budgets, she added, referring to the next Multiannual Financial Framework (MFF), the long-term EU budget for 2028-2034.

The auditors selected a sample of ten Member States (Austria, Bulgaria, Estonia, France, Germany, Latvia, Malta, the Netherlands, Romania, and Spain), representing different shares of total RRF funding as a percentage of national GDP. In addition, they surveyed all 27 Member States.

They examined whether the EU’s legal framework provides for minimum traceability requirements, if the Member States trace the use of funds and collect the required data, and if they and the Commission make use of actual cost data to update cost estimates, reallocate funds and properly assess the RRF’s efficiency. The answers to these questions were mostly negative.

Value for money?

The ECA concluded that whether the RRF delivers value for money cannot be assessed. This contradicts Article 317 in the EU Treaty, which states that the Commission, when implementing the budget, shall have regard to the principles of "sound financial management".

Article 33 in the Financial Regulation states that this overriding concept in the management and control of the EU budget comprises the principles of economy, efficiency and effectiveness. The principle of efficiency concerns the best relationship between the resources employed, the activities undertaken and the achievement of objectives.

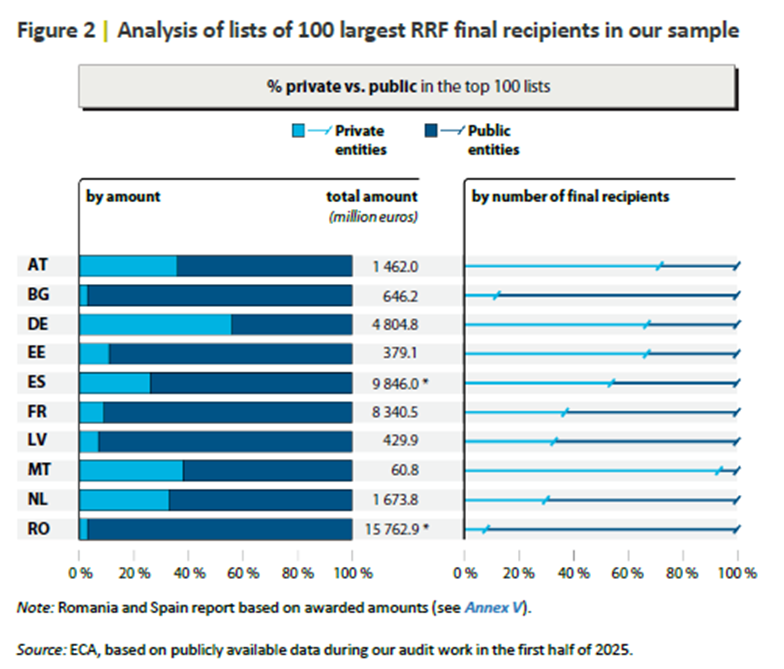

EU Member States are required to publish the 100 largest final recipients of the EU funding of the RRF. The ECA found that 50% of them are public bodies, accounting for over 80% of the amounts, and not those that actually have spent the money.

The 100 largest final recipients in the sample of 10 EU Member States. Credit: ECA

The ECA concludes that publishing information just on the 100 largest final recipients of RRF funding does not properly capture the overall use of the funds because the RRF Regulation does not extend the publication obligation to contractors. There were also variations in how the Member States are collecting and disclosing spending data.

Four countries in the sample collected actual cost data on final recipients, including subcontractors, showing that this is possible. The other four countries only did it upon request, but not always: France and Germany provided the list of measures and the total amount received, without breaking it down at the level of each measure.

The French authorities were not able to provide the names of final recipients for three of the five measures sampled. They told the auditors that this was because it was too administratively burdensome to obtain information on final recipients and amounts paid for some measures, even upon request.

The transparency gap

In previous audits on the "accountability gap", the Commission disagreed with the ECA. It was hardly expected that it would agree about the "transparency gap" which was the focus of the new audit.

"For us, the key point is not whether the Commission agrees with us or not," Maletić told The Brussels Times. "We are auditors, and the Commission is our auditee. Our role is to identify where systems do not meet principles of sound financial management, good practice, and established standards – and to clearly indicate what needs to be improved."

The main point of disagreement with the Commission concerns financing not linked to costs, she explained. "The Commission considers that, under such instruments, there is no obligation to systematically collect and report information on actual costs and final beneficiaries. We do not share this view."

"We have consistently called for reporting on actual costs as a necessary element for managing the funds and assessing value for money. There is no obligation in the RRF regulation, but the Commission is obliged, according to the financial regulation, to collect cost data. If you want to assess value for money, you need to know the actual costs."

The audit did not directly measure public trust. However, based on interactions with stakeholders – in particular discussions in the European Parliament on its RRF reports – the ECA observed a significant increase in concerns related to transparency. "We have not previously experienced such a level of persistent questioning and scepticism regarding the use of EU public funds," she said.

While the ECA had considered engaging the national audit offices in the Member States in a parallel audit of the transparency issue, Maletić said that they decided not to go through with it. "Our experience with audit cooperation with them in the past has been positive but limited, and we are also aware that it could become a risk factor leading to delayed publication times."

That said, the supreme audit institutions (SAIs) from the sampled Member States were invited to the ECA’s audit meetings. She hopes that the SAIs in the Member States will launch their own audits of the RRF, based on the ECA’s audit.

The auditors noted both overspending and savings in the audit. They found that out of 19 measures in the audited sample, 15 experienced cost savings, typically ranging between 7% and 25%, while four measures experienced cost overruns.

"We think that a full view of where the measures stand in terms of savings and overruns would allow for timely reallocations between measures to achieve the fulfilment of their objectives," they said.

Disagreement with the Commission

The auditors did not try to estimate the cost overruns and possible savings. "This exercise can only be carried out once the RRF is fully implemented and actual costs are known. Quantification of possible losses is not possible as long as measures are still running until December 2026." The audit covered the period from the RRF’s inception in February 2021 to mid-2025.

"The overruns do not necessarily indicate possible fraud or irregularities," she pointed out. "We have no indication of this from any of the evidence we collected. As we explain in the report, we are aware of other factors that appear to have led to overruns: high levels of inflation, persistent post-pandemic supply chain issues, and energy crises."

The ECA concluded the report with three principal recommendations targeting both the RRF and any future EU instrument that may be implemented based on "financing not linked to costs".

In its reply, the Commission, not surprisingly, rejected the recommendations.

In a press statement, the Commission summarised that it "maintains that the RRF’s legal framework ensures accountability through robust transparency measures".

As regards the audit recommendations, it wrote that it "cannot endorse their implementation" because the RRF Regulation "already strikes a balance between enhanced transparency and minimising administrative burdens".